Corn Trade Dynamics – February ,2025

Global Supply & Demand Outlook (2024-25)

Despite supply risks in some regions, the global corn balance is expected to remain resilient.

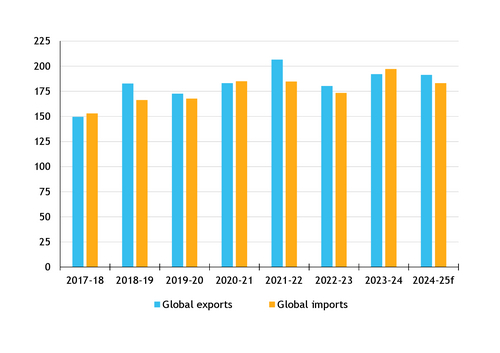

The USDA projects total global supply to exceed global imports by 7 million metric tons (Mt), providing a buffer against shortfalls.

- Total global corn exports for 2024-25 are forecasted to decline slightly to 191.4Mt.

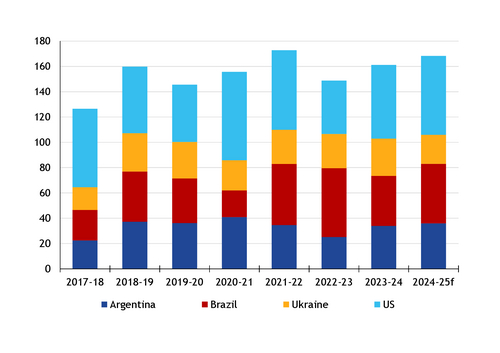

- Argentina, Brazil, and the U.S. are collectively expected to boost their exports to 145.2Mt, up from 131.7Mt the previous year.

- U.S. corn exports are set to rise by 4Mt to 62.2Mt, while Argentina’s exports are projected to increase by 2Mt to 36Mt.

- Brazil will see the highest growth, with exports forecasted to rise 7.5Mt to 47Mt.

- Ukraine’s exports, in contrast, are expected to fall by 6.5Mt to 23Mt, following a production decline to 26.5Mt.

Competitive Struggles in the Corn Market

Ukrainian corn faces increasing challenges in global trade, struggling to compete against major suppliers such as the U.S., Argentina, and Brazil. Domestic producers have been holding back supplies in anticipation of price rebounds, limiting export flows.Ukraine’s share in the global corn market is projected to decline due to a downturn in both production and exports for the 2024-25 season.

Meanwhile, the world’s leading exporters—Argentina, Brazil, and the U.S.—are expected to expand their export volumes.

Since December, Ukraine’s corn shipments have decelerated, constrained by reduced availability and uncompetitive pricing relative to its South American and U.S. counterparts. This hesitation in price flexibility has hindered Ukraine from fully capitalizing on market fluctuations.

- Ukrainian producers tend to raise their price expectations whenever global prices increase, making their exports less attractive.

- Conversely, when prices decline, producers often withhold supply, anticipating future rebounds.

- This pattern frequently results in delayed sales, with hopes of leveraging seasonal price support, particularly from potential production risks in Argentina or Brazil.

Losing Market Share in China

Brazil and the U.S. are increasing their competitiveness in the Chinese corn market, posing additional pressure on Ukrainian exports. Compounding the issue, China’s total corn demand is projected to decline sharply in 2024-25, forcing Ukraine to seek alternative buyers.

U.S. Gaining Presence in Spain

The U.S. has expanded its footprint in Spain’s corn import market, securing commitments totaling 942,600Mt as of mid-January—already exceeding the 711,000Mt total U.S. exports to Spain from the previous marketing year.

Competition with Argentina in Egypt

Egypt has traditionally been a significant importer of Ukrainian corn, but Argentina remains a key rival in this market. However, Argentina’s 2024-25 crop is at risk due to adverse weather, and Egyptian buyers have increasingly turned to Brazil and the U.S. as alternative suppliers.

If Argentina experiences further production losses, global prices may rise, but Ukrainian producers are likely to increase their price expectations, further reducing their competitiveness.

Brazil’s May Harvest , and Impact on Global Corn Trade

Brazil’s new corn crop is expected to enter global markets by May 2025, adding fresh supply to key destinations including Egypt, China, Spain, and Portugal.

If Brazilian production remains on track, Ukrainian exports will struggle to compete with Brazil’s ample and competitively priced supply.

Strategic Takeaways for Market Participants

- Monitor global price trends and Ukraine’s price positioning to assess potential trade opportunities.

- Watch speculative positioning (COT) for insights into market sentiment.

- Assess Argentina’s weather conditions, as further production losses could shift trade flows.

- Evaluate China's declining import demand, as it may create surplus volumes for other buyers.

- Prepare for Brazil’s upcoming harvest, which could pressure global prices and impact Ukraine’s competitiveness.

For customized market intelligence and trading strategies, contact GrainFuel Nexus® for tailored insights.

GrainFuel Nexus® will continue to provide real-time updates as new trends emerge.

GrainFuel Nexus® | Expert Commodity Intelligence & Strategic Advisory

Subscribe to our Strategic Reports - Essential Dive & Deep Dive Advisory